Business Validation Tip #1: Explain the Problem and Opportunity

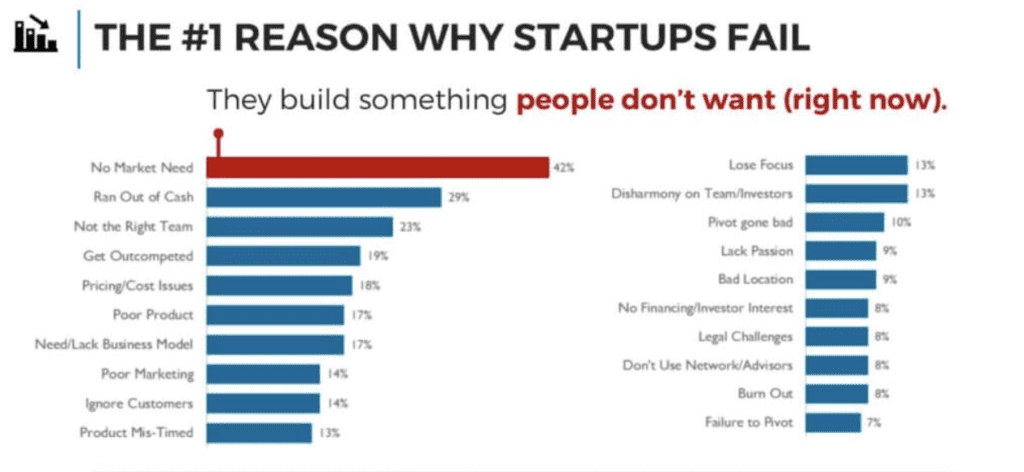

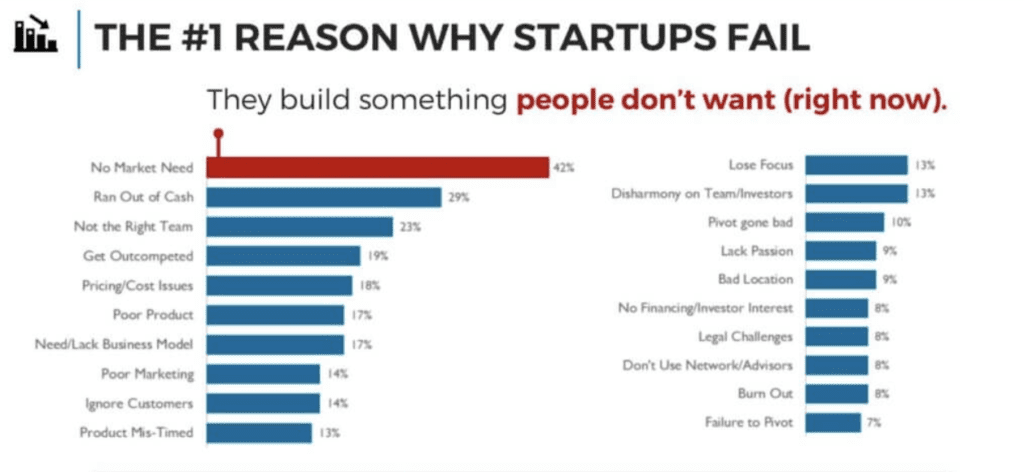

This is always the first thing that you need to do. You must be able to clearly articulate the problem that you’re trying to solve as well as the opportunity at hand. The number one reason why startups fail is because the market doesn’t need what they’re offering. You must be able to clearly identify the problem and opportunity in the market. If you can’t do that, it might be time to go back to the drawing board and create a new business plan for your software development venture.

Conduct market research. Get your market validation. What is the market looking for? Is there an existing need that you’re trying to fill? Or are you creating a new need?

If you’re addressing an existing need, this can be split up into two categories—needs that you have and needs that others have.

If you don’t feel the need yourself, the product might suffer a little bit. That’s because the information you’re getting is always one step removed.

The other side of this concept is creating a completely new demand. This is extremely difficult but highly profitable.

Smartphones are the perfect example to explain what I mean.

If you’re old enough to remember, think about the days when nobody had smartphones. We were all just fine. Life continued and operated with no problems.

But now I dare you to put your smartphone down and walk to the end of the block. See what happens. You’ll get anxious, and the addiction to your phone will start to kick in. You need to be with your phone at all times.

This type of need didn’t exist prior to the invention of the smartphone. But once it was created, the need was established.

So if a product can create a new need or functionality, you have the opportunity for limitless profits, but it’s extremely risky.

The next thing that you need to ask yourself is whether your business idea is a “must-have” or “nice to have” product. Is it a consumer luxury item? Or can people do without it?

The loyalty of your customers will differ based on whether or not this is a need or a want.

You must be able to clearly identify the problem and opportunity in the market. If you can’t do that, it might be time to go back to the drawing board and create a new business plan for your software development venture.

Conduct market research. Get your market validation. What is the market looking for? Is there an existing need that you’re trying to fill? Or are you creating a new need?

If you’re addressing an existing need, this can be split up into two categories—needs that you have and needs that others have.

If you don’t feel the need yourself, the product might suffer a little bit. That’s because the information you’re getting is always one step removed.

The other side of this concept is creating a completely new demand. This is extremely difficult but highly profitable.

Smartphones are the perfect example to explain what I mean.

If you’re old enough to remember, think about the days when nobody had smartphones. We were all just fine. Life continued and operated with no problems.

But now I dare you to put your smartphone down and walk to the end of the block. See what happens. You’ll get anxious, and the addiction to your phone will start to kick in. You need to be with your phone at all times.

This type of need didn’t exist prior to the invention of the smartphone. But once it was created, the need was established.

So if a product can create a new need or functionality, you have the opportunity for limitless profits, but it’s extremely risky.

The next thing that you need to ask yourself is whether your business idea is a “must-have” or “nice to have” product. Is it a consumer luxury item? Or can people do without it?

The loyalty of your customers will differ based on whether or not this is a need or a want.

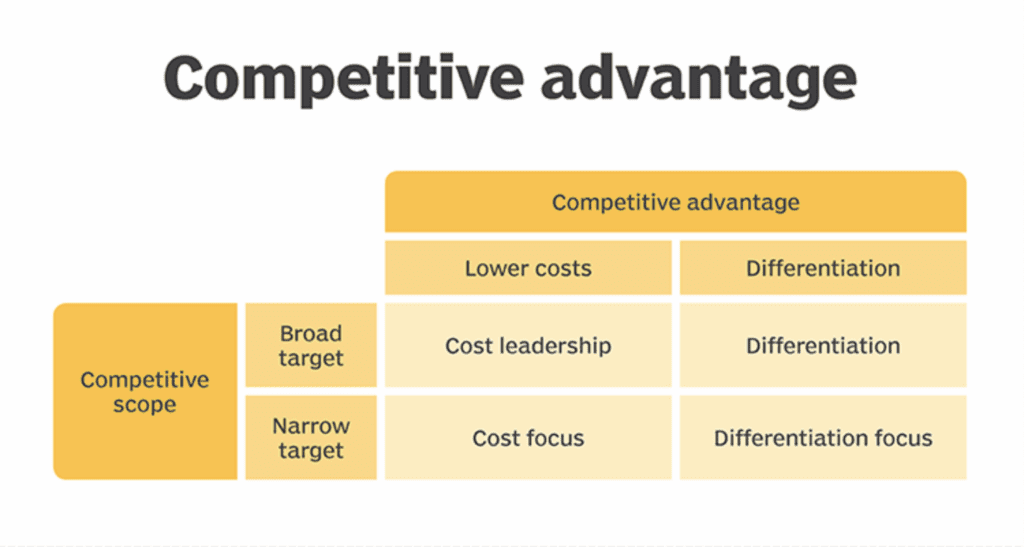

Business Validation Tip #2: Competitive Advantage Analysis

Once you’ve identified the market need, you must be able to properly articulate your competitive advantage. If you’re entering an existing market that has competitors, why should the target audience pick you over the competition? There must be a differentiator in your product that improves the user experience. What is your competitive advantage? If you’re just another “me too” business, then you’re not different. Your idea must be different enough to stand out from the crowd. Give people a reason to choose you over the other players in the market.

You need to develop a strategy for how you’re going to beat your competitors. Play to win.

The strategy must explain how you’re going to gain ground on the competition. They’ve already been in business for months, years, or potentially decades before you. So you have lots of ground to cover just to catch up; then you can beat them from there.

Your idea must be different enough to stand out from the crowd. Give people a reason to choose you over the other players in the market.

You need to develop a strategy for how you’re going to beat your competitors. Play to win.

The strategy must explain how you’re going to gain ground on the competition. They’ve already been in business for months, years, or potentially decades before you. So you have lots of ground to cover just to catch up; then you can beat them from there.

Business Validation Tip #3: Is Your Idea Defendable?

If you don’t have any competitors, and you’re creating something new, then you need to ask yourself this—”is my idea defendable?” Here’s what I mean by defendable. Does your product have intellectual property that you can patent to defend against other competitors? In software, a patent is super easy to obtain and extremely difficult to defend. This is a common question that I hear from all of my clients. It’s such a common occurrence that I’ll probably write a complete guide on the topic soon. With software, everyone asks, “Can I patent it?” The answer is yes. But the real question should be, can you defend it? And the answer—you probably can’t. All someone else needs to do is change 20% of your patent, and it’s considered to be different software by law. It’s much easier to defend a utility patent if you’re an electrical engineer or something like that. But when you’re dealing with software, intellectual property is extremely hard to defend. So there could be other app developers or app development companies out there creating solutions for the app store with the same functionality as your software. Think about the electric scooters that we see popping up in all major cities right now. It’s a really good idea, and it’s already out there. However, it’s so difficult to defend. Within months there are three or four other competitors coming to join the party. Delivery apps available for iOS and Android apps are another example. A mobile app development company or freelancer could create a successful app without another app business in the delivery space getting in their way. There are just two examples of great application ideas that are tough to defend.Business Validation Tip #4: Go to Market Strategy

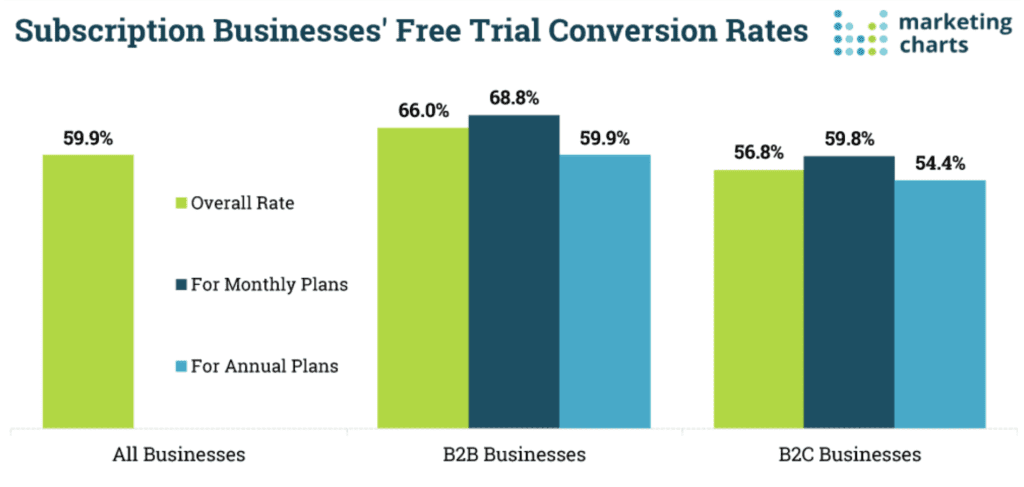

In terms of business validation for your tech startup idea, you must have a very specific go-to-market strategy. What do I mean by this? When you develop a product or a business, and you’re ready to open up your doors, start selling, taking subscriptions, or whatever else you’re offering—how does the world know that you exist? How are you going to start gaining customers? If you’re a brick and mortar company, you can do this through guerilla marketing. Make some posters and take out local ads. Maybe you’re in a high traffic area, and people will just randomly see you. That’s fine for brick and mortar, but technology is a bit different. You could have the best idea and the wold that nobody has heard about. So you need to have a marketing strategy. Always reserve some of your funds to make sure you have some sort of digital marketing presence. You might start by creating an MVP (minimum viable product) for your mobile application and promote it via social media. Consider offering some type of freemium model. Allow people to try your product before they actually purchase anything. Free trials for subscription businesses have a historically high conversion rate. Lots of times, this strategy will be much cheaper than a full-blown marketing plan. You’ll still need to have some marketing to let people know that there’s a free tier, but it won’t be as involved.

When it comes to your go-to-market strategy, there are lots of different ways to approach this. There is an age-old question for a scenario that shows two different schools of thought.

Let’s say there is a town with two successful Italian restaurants. People love Italian food in this town, and everyone goes to both. You decide to open up a brand new restaurant. Do you open an Italian one? Or something else?

One school of thought says that you already know how much people love Italian food here. If you can do a better job than the others, you’ll be successful.

The other school of thought says that this town is already saturated with Italian food. But obviously, people enjoy going out to eat. You can open up a restaurant offering a different type of cuisine to be successful.

Which method is correct? Drop a comment and let me know what you think.

Lots of times, this strategy will be much cheaper than a full-blown marketing plan. You’ll still need to have some marketing to let people know that there’s a free tier, but it won’t be as involved.

When it comes to your go-to-market strategy, there are lots of different ways to approach this. There is an age-old question for a scenario that shows two different schools of thought.

Let’s say there is a town with two successful Italian restaurants. People love Italian food in this town, and everyone goes to both. You decide to open up a brand new restaurant. Do you open an Italian one? Or something else?

One school of thought says that you already know how much people love Italian food here. If you can do a better job than the others, you’ll be successful.

The other school of thought says that this town is already saturated with Italian food. But obviously, people enjoy going out to eat. You can open up a restaurant offering a different type of cuisine to be successful.

Which method is correct? Drop a comment and let me know what you think.

Business Validation Tip #5: Financial Forecast and Security

You need a very clear financial statement and forecast of how your company is going to operate when it’s losing money in the beginning. When you first start, you’ve spent lots of money and don’t have any customers. You need to figure out when you’re going to go from red to black, which is your breakeven point. Then figure out when you’re going to turn profitable and get into the green. How is this going to happen? How long will it take? If you don’t know the answer to these questions, then you won’t know how much cash you need in your reserves. How much funding will you need to survive the storm? So many businesses fail, not because the idea was bad—they just ran out of fuel. They didn’t calculate how long they needed to stay in the market to gather enough critical mass to become profitable. Remember the graph I showed you earlier about the top reasons why startups fail? I already highlighted the fact that “no market need” ranked first on that list. But let’s look at it again and see some of the other reasons. Running out of cash is the second most common reason why startups fail.

If you’re in the technology field, you hear about lots of companies operating at a loss on a massive scale until they become profitable.

Think of companies like Amazon. They didn’t make money for the longest time until they dominated the entire market. Think of companies like Twitter or LinkedIn. They lost money for years, and some are still losing money and not profitable.

You need to address these types of scenarios. What type of company are you going to be?

All development costs must be taken into consideration for your new app.

There’s a different strategy from user adoption to profitability that needs to be played out on paper before your company goes live. What’s your monetization strategy? Outline a Plan A, Plan B, and Plan C, so you have some contingencies in order.

The financial aspects of your project will be crucial if you’re trying to raise money from potential investors beyond crowdfunding.

Running out of cash is the second most common reason why startups fail.

If you’re in the technology field, you hear about lots of companies operating at a loss on a massive scale until they become profitable.

Think of companies like Amazon. They didn’t make money for the longest time until they dominated the entire market. Think of companies like Twitter or LinkedIn. They lost money for years, and some are still losing money and not profitable.

You need to address these types of scenarios. What type of company are you going to be?

All development costs must be taken into consideration for your new app.

There’s a different strategy from user adoption to profitability that needs to be played out on paper before your company goes live. What’s your monetization strategy? Outline a Plan A, Plan B, and Plan C, so you have some contingencies in order.

The financial aspects of your project will be crucial if you’re trying to raise money from potential investors beyond crowdfunding.

Business Validation Tip #6: Does Your Business Scale?

You must be able to explain how your company and idea can scale. If your company is relying on you and your skillset—you don’t scale. There are only 24 hours in a day. No matter what happens, you can’t add a 25th hour. Do your costs decrease over time and volume? Do your costs plateau? Do your costs increase? Some business models are fundamentally flawed from the beginning because they are assuming a fixed cost structure, which is not correct. At scale, your company will have different logistics. Sometimes one employee can wear several different hats. But at scale, you’ll still need multiple employees. Your costs will go up. If you’re housing all of your products locally at your office, that’s fine for now. But what happens when you scale and need to rent or buy a warehouse? Your costs will go up. Make sure you play out different scenarios to understand how the idea works at scale. You also need to identify whether your product and company can cross demographics and markets. If you saturate a particular market, is there a lateral move you can make to gain more customer adoption?BONUS Tip for Business Validation: Versatility and Resilience

This is more of a long term plan and strategy, but you should be thinking about it from the beginning. Is your company versatile and resilient? Think of companies like Borders and Barnes & Noble. They’ve become completely obsolete. They had the opportunity to potentially go digital with selling books, but their efforts were too little and too late. Another great example is car alarm companies. The car alarm itself hasn’t become obsolete. But now all of the car manufacturers build them directly into vehicles. So consumers don’t need to buy an after-market alarm. All of those businesses that opened up to sell car alarms are now obsolete. Think about accessories for iPhones. Each accessory is so specific for adaptors. Once Apple changes the adaptors for new iPhones, all of your inventory becomes worthless. This is a serious problem if you have a large warehouse full of accessories that can’t be used. So the question becomes when (not if) something hits your market, are you versatile enough to adjust and shift? Do you have the foresight to make adjustments ahead of time? Can you adapt to ever-changing markets?Conclusion

Take all of these tips that I’ve explained above and use them to develop your business idea. Be as truthful with yourself as possible. Maybe vet your best app idea out with some friends. See if there’s anything you forgot or missed. It’s always helpful to get another perspective on things that you might not see on your own. It’s extremely important to adjust now so your business can see success. Just because you find a hurdle, it doesn’t mean that you have a bad idea. Sometimes you just need to reshape that idea or rethink your strategy to be successful. It’s much cheaper to make these adjustments now compared to after you build your company. I hope this guide was helpful in explaining how to validate your business idea. Now you can hit the market and be successful at everything that you do.Frequently Asked Questions

How can I validate my mobile app idea effectively?

To validate your mobile app idea, start by clearly articulating the problem and opportunity it addresses. Conduct thorough market research to ensure there is a demand.

What are the key components of a go-to-market strategy for a tech startup?

A go-to-market strategy should include a clear marketing plan, budget allocation for digital presence, and possibly a freemium model to attract initial users.

How do I determine if my app idea has a competitive advantage?

Identify what makes your app unique compared to existing solutions. This could be a feature, user experience, or pricing model.

Is it possible to patent a mobile app idea?

While you can patent a mobile app, defending it can be challenging. Software patents are often easy to obtain but difficult to enforce, as competitors can make minor changes to bypass them.

What role does market research play in app development?

Market research is crucial in app development as it helps identify user needs, validate demand, and refine the app’s features to better meet market expectations.